How Much House Can You Really Afford in the Philly Suburbs?

A 2026 Mortgage-Rate & Income Guide

Summary

One of the biggest mistakes home buyers make in the Philadelphia suburbs is confusing what a lender will approve with what they can actually afford. In 2026, with higher interest rates, rising property taxes, and big price gaps between the Main Line, Bucks County, and Chester County, that difference can be hundreds of thousands of dollars.

This guide explains how to calculate your true buying power, how mortgage rates and taxes change the math, and how much house different income levels realistically support across the Philly suburbs.

Table of Contents

Why 2026 Affordability Is So Different

What Lenders vs. Households Think “Affordable” Means

The Four Costs That Matter

How Interest Rates Multiply Prices

Property Taxes in the Philly Suburbs

Income vs. Home Price: Realistic Ranges

Main Line vs Bucks vs Chester County

Down Payments and Their Hidden Power

What Buyers Get Wrong

A Smart Affordability Framework

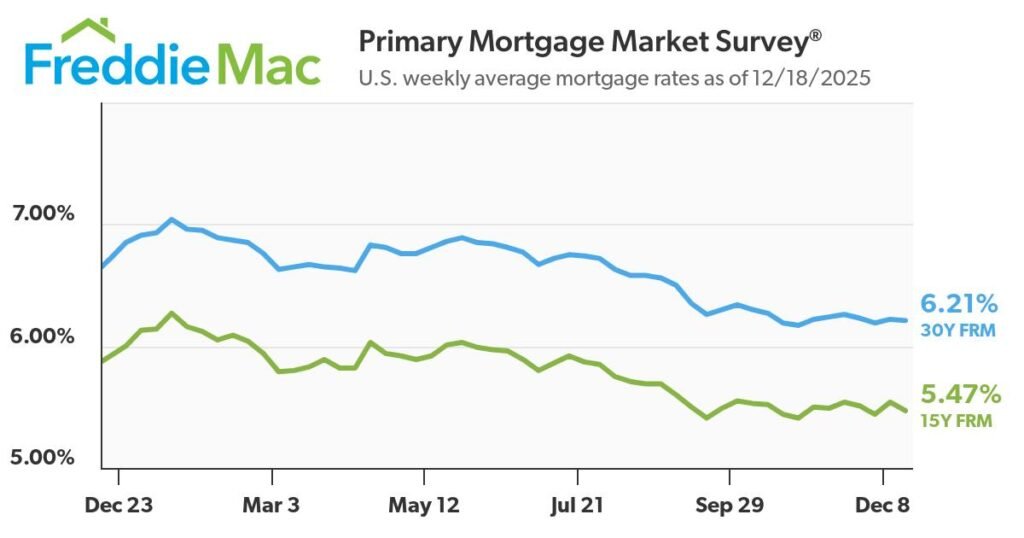

1. Why 2026 Affordability Is So Different

Today’s buyers are dealing with a housing market that looks nothing like the 2019–2021 era.

Prices are still elevated.

Mortgage rates are materially higher.

Taxes and insurance have increased.

That means monthly payments — not just home prices — determine what you can buy.

A $750,000 home in 2026 can cost more per month than a $1,000,000 home did just a few years ago.

2. What Lenders vs. Households Think “Affordable” Means

Lenders will typically approve buyers for payments up to:

• 43–50% of gross monthly income

But that does not mean it is financially healthy to spend that much.

Most households are comfortable closer to:

• 25–35% of gross income

The difference is the line between living well and feeling house-poor.

3. The Four Costs That Matter

Your true housing cost includes more than your mortgage.

You must budget for:

• Principal & interest

• Property taxes

• Homeowner’s insurance

• HOA or maintenance

Ignoring any of these can blow up your budget.

In the Philly suburbs, taxes alone can equal the payment on a small condo.

4. How Interest Rates Multiply Prices

Rates don’t just change your payment — they change what price you can afford.

A one-point change in interest rates can shift buying power by 10–15%.

That means two buyers with the same income, buying in different rate environments, can afford drastically different homes.

This is why 2026 buyers must be more strategic than 2020 buyers ever were.

5. Property Taxes in the Philly Suburbs

Taxes vary dramatically by township and school district.

A $700,000 home might have:

• $6,000/year in one town

• $12,000+ in another

That difference alone can swing affordability by over $500 per month.

This is why comparing homes across Lower Merion, Radnor, Central Bucks, and Downingtown without adjusting for taxes is misleading.

6. Income vs. Home Price: Realistic Ranges

While every household is different, these are rough comfort-zone guidelines for 2026 buyers:

| Household Income | Comfortable Home Price |

|---|---|

| $150,000 | $500,000 – $650,000 |

| $200,000 | $650,000 – $850,000 |

| $250,000 | $850,000 – $1,100,000 |

| $300,000+ | $1M – $1.4M+ |

These assume strong credit, moderate taxes, and typical down payments.

7. Main Line vs Bucks vs Chester County

Where you buy dramatically changes what your income can support.

Main Line

Higher prices, higher taxes, tighter inventory. Buyers often need $250K+ income to compete for family homes.

Bucks County

More options under $800K. Strong schools available at lower price points.

Chester County

Wide range. West Chester and Downingtown offer value compared to Radnor and Lower Merion.

Same income, different zip codes — wildly different outcomes.

8. Down Payments and Their Hidden Power

Down payments don’t just reduce loan size — they change everything.

A larger down payment:

• Lowers monthly payment

• Reduces mortgage insurance

• Improves loan terms

• Expands price range

Two buyers earning the same income but putting 10% vs 30% down live in completely different housing worlds.

9. What Buyers Get Wrong

Most buyers:

• Max out their pre-approval

• Ignore taxes and insurance

• Assume rates will fall

• Underestimate maintenance

• Overestimate lifestyle tolerance

This leads to regret, not equity.

10. A Smart Affordability Framework

Before house hunting, determine:

• Comfortable monthly payment

• Down payment available

• Tax tolerance by township

• Long-term lifestyle goals

Then work backward to price.

The best buyers are not the ones who stretch — they’re the ones who buy homes they can easily hold through any market.