Is Renting Really “Throwing Money Away”?

A Smarter Way to Think About Rent vs. Buy

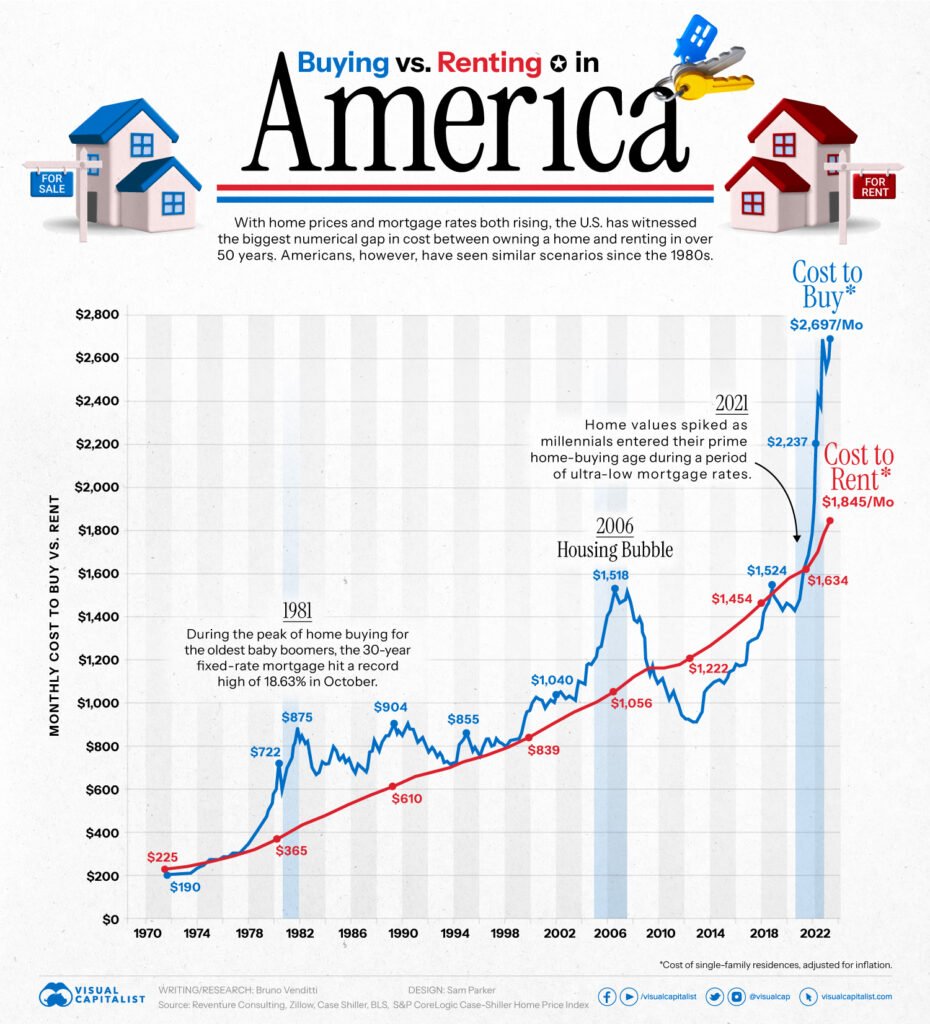

Summary

Few phrases in real estate are repeated as casually — and as inaccurately — as “renting is throwing money away.” The statement is emotionally powerful, but it’s also incomplete. In practice, the rent-vs-buy decision is less about ideology and more about timing, flexibility, cash flow, and risk tolerance.

In markets across Bucks County and Chester County — from Doylestown and Newtown to West Chester, Malvern, and Downingtown — buyers face real trade-offs. For some, buying is absolutely the right move. For others, renting is not only rational, but strategically sound.

This article reframes the conversation so you can decide based on outcomes, not slogans.

Table of Contents

Why “Throwing Money Away” Is the Wrong Frame

What Rent Actually Buys You

The Hidden Costs of Ownership

Time Horizon Matters More Than Price

Flexibility vs. Forced Savings

Market Volatility and Emotional Risk

Local Context: Bucks and Chester County Examples

When Buying Clearly Wins

When Renting Is the Smarter Choice

The Strategic Takeaway

1. Why “Throwing Money Away” Is the Wrong Frame

Rent is not an investment — but neither is much of what we spend money on.

Rent buys:

shelter

predictability

flexibility

limited liability

Calling rent “wasted” assumes that ownership automatically produces better financial outcomes. That assumption only holds under specific conditions — not universally, and not at every point in life.

The better question is not “Am I building equity?”

It’s “What am I buying with my housing choice — and what am I giving up?”

2. What Rent Actually Buys You

Renting provides:

fixed monthly costs (at least within the lease term)

insulation from repair and capital expenses

geographic flexibility

time flexibility

For professionals relocating, changing careers, or testing new areas — such as moving from Philadelphia into towns like Doylestown or West Chester — renting can function as paid reconnaissance, not wasted money.

That optionality has value.

3. The Hidden Costs of Ownership

Ownership builds equity — but it also introduces costs that are easy to underestimate:

maintenance and repairs

capital expenditures (roof, HVAC, windows)

transaction costs

opportunity cost of tied-up cash

emotional stress during market downturns

In Bucks and Chester County, where housing stock ranges from historic homes to newer developments, maintenance variability is real. Two homes at the same price point can produce very different ownership experiences.

Those costs don’t show up in mortgage calculators — but they affect outcomes.

4. Time Horizon Matters More Than Price

Ownership rewards time.

Buying generally makes sense when:

you plan to stay long enough to amortize transaction costs

you’re comfortable riding out market cycles

your income is stable

Short time horizons amplify risk. If you’re unsure whether you’ll stay in Newtown or Malvern for three years or ten, renting may preserve flexibility while clarity develops.

Time is the silent variable most people ignore.

5. Flexibility vs. Forced Savings

One argument for buying is forced savings — paying down principal instead of rent.

That’s real. But it comes with trade-offs:

reduced liquidity

reliance on home value appreciation

inflexibility if circumstances change

Some renters save aggressively while renting. Others don’t. The difference isn’t rent vs. buy — it’s behavior.

Ownership doesn’t guarantee discipline. Renting doesn’t preclude it.

6. Market Volatility and Emotional Risk

Buying introduces emotional exposure to market movements.

When prices soften:

owners feel trapped

life decisions become constrained

stress increases

Renters experience market changes differently. They may face rent increases, but they’re not tied to a single illiquid asset.

In transitional markets — or when interest rates fluctuate — renting can act as a volatility buffer rather than a failure to commit.

7. Local Context: Bucks and Chester County Examples

In towns like Doylestown or West Chester, demand is strong and long-term fundamentals are solid. Buying can make sense if:

you’re aligned with the community

schools, commute, and lifestyle fit

you’re comfortable with the price point

In faster-moving or more heterogeneous areas — parts of Downingtown or Malvern, for example — renting first can help buyers learn block-by-block differences before committing capital.

Local nuance matters more than national headlines.

8. When Buying Clearly Wins

Buying is often the better choice when:

you have a stable long-term plan

the payment is comfortable, not stretched

the home meets both present and future needs

you can absorb repairs without stress

In these cases, ownership can provide:

equity growth

stability

emotional satisfaction

The key is that the decision works even if appreciation slows.

9. When Renting Is the Smarter Choice

Renting is often the better choice when:

your timeline is uncertain

your income may change

you’re relocating or testing a market

buying would strain cash flow

In these situations, renting is not avoidance — it’s strategic patience.

10. The Strategic Takeaway

Renting and buying are tools, not moral positions.

A good housing decision:

aligns with your timeline

preserves flexibility where needed

doesn’t rely on perfect conditions to succeed

The mistake isn’t renting. The mistake is buying for the wrong reasons — pressure, fear, or slogans — rather than structure.

Closing Thought

Renting isn’t throwing money away. It’s paying for flexibility and time.

Buying isn’t always building wealth. It’s taking on risk in exchange for potential upside.

The smartest decision is the one that still makes sense if life changes — because eventually, it will.

By Eric Kelley, Philadelphia Suburbs Realtor & Attorney