The Hidden Costs of Homeownership First-Time Buyers Don’t Budget For

Summary

Most first-time buyers spend months preparing for a down payment and mortgage — but far less time preparing for the ongoing costs of owning a home. The result is a familiar pattern: buyers qualify comfortably on paper, close with confidence, and then feel financial pressure within the first year.

This isn’t because they bought irresponsibly. It’s because many of the true costs of homeownership are invisible during the buying process, especially in markets like the Philadelphia suburbs, where taxes, maintenance, and municipal structures vary widely by location.

This article breaks down the hidden costs first-time buyers often underestimate — and how to budget realistically so ownership feels sustainable, not stressful.

Table of Contents

Why First-Time Buyers Underestimate True Costs

Property Taxes: More Than a Line Item

Home Maintenance Isn’t Optional (or Cheap)

Repairs That Don’t Feel Like “Repairs”

Utilities and Energy Costs

Insurance Gaps and Surprises

HOA Fees and Special Assessments

Furniture, Tools, and “Setup” Costs

Transactional Costs After Closing

A Smarter Budgeting Framework

1. Why First-Time Buyers Underestimate True Costs

Most first-time buyers anchor to the monthly mortgage payment. That makes sense — it’s the largest and most visible expense. But ownership costs extend far beyond principal and interest.

Buyers underestimate costs because:

Rent includes many expenses ownership does not

Lenders focus on qualification, not comfort

Online calculators simplify reality

Many costs are irregular, not monthly

The danger isn’t one big surprise — it’s the cumulative effect of smaller, recurring expenses that don’t show up in pre-approval conversations.

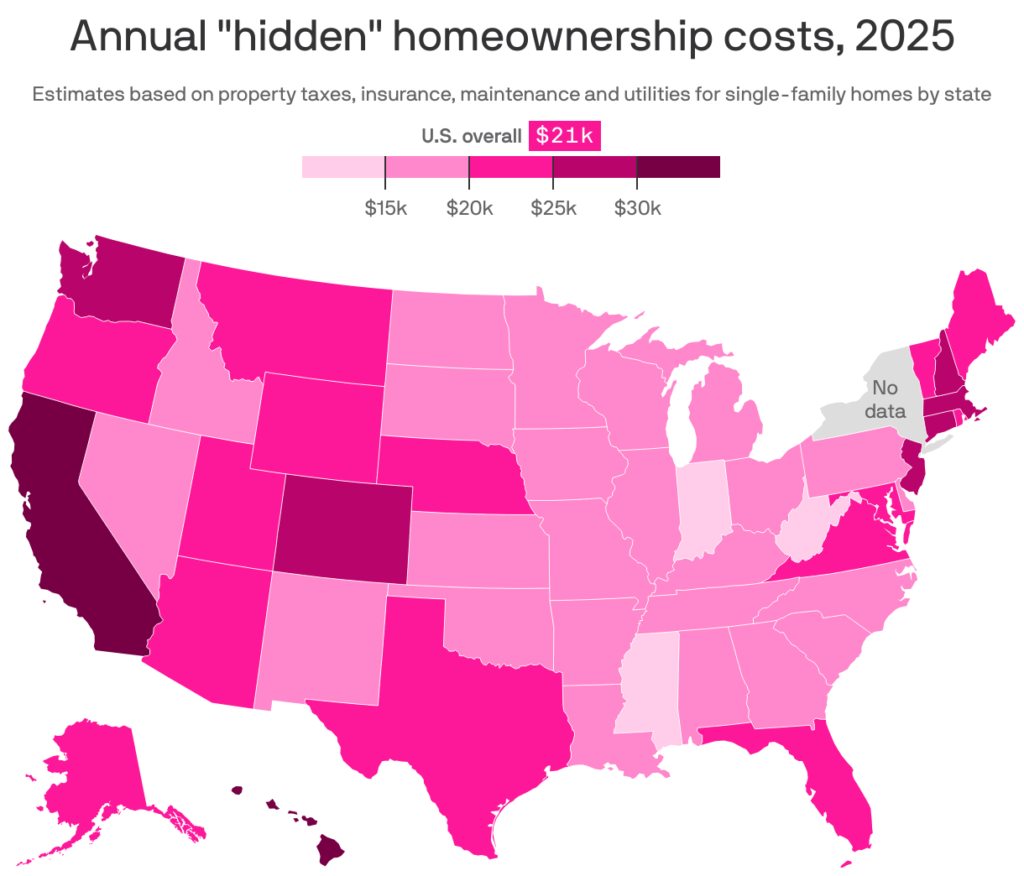

2. Property Taxes: More Than a Line Item

Property taxes are one of the most misunderstood ownership costs.

Common mistakes include:

Assuming taxes won’t change after purchase

Ignoring reassessment risk

Comparing list prices without comparing tax burdens

In the Philly suburbs, two similar homes can have:

Identical purchase prices

Radically different tax bills

Taxes affect:

Monthly escrow payments

Long-term affordability

Resale competitiveness

Buyers should always evaluate taxes as part of total monthly ownership cost, not as an afterthought.

3. Home Maintenance Isn’t Optional (or Cheap)

A common rule of thumb is to budget 1%–2% of a home’s value per year for maintenance. Many first-time buyers ignore this entirely.

Maintenance includes:

HVAC servicing

Gutter cleaning

Landscaping

Minor plumbing and electrical work

Appliance upkeep

Even in well-maintained homes, these costs add up. And unlike rent, maintenance costs are your responsibility — whether or not you planned for them that month.

4. Repairs That Don’t Feel Like “Repairs”

Some of the most expensive ownership costs don’t feel like repairs — but they are.

Examples include:

Replacing a water heater

Addressing drainage issues

Fixing roof leaks before failure

Updating aging electrical panels

These costs often appear suddenly and demand immediate attention. Buyers who budget only for visible repairs are often caught off guard by system-related expenses.

5. Utilities and Energy Costs

Utility costs are frequently underestimated — especially by buyers moving from apartments or smaller homes.

Ownership often means:

Larger square footage

Less insulation efficiency in older homes

Outdoor water usage

Seasonal heating and cooling swings

Monthly utility bills can vary dramatically by:

Home size

Age

Construction quality

Fuel source

A mortgage payment may be fixed, but utility costs are not.

6. Insurance Gaps and Surprises

Homeowners insurance is another area where buyers often budget inaccurately.

Beyond base premiums, buyers may encounter:

Higher premiums for older homes

Increased costs for certain roof types

Separate flood insurance

Coverage gaps for valuables or home offices

Insurance costs can also rise over time, especially after claims or regional risk reassessments.

7. HOA Fees and Special Assessments

For buyers purchasing townhomes or properties with associations, HOA costs are often misunderstood.

HOA fees may cover:

Exterior maintenance

Roofs and siding

Landscaping and snow removal

Amenities

However, buyers should also understand:

What the HOA does not cover

Whether reserves are adequate

The risk of special assessments

A low monthly fee can be misleading if the association is underfunded.

8. Furniture, Tools, and “Setup” Costs

One of the most overlooked costs of ownership is simply making the house functional.

First-time buyers often need to purchase:

Furniture sized for the new space

Lawn equipment

Basic tools

Window treatments

Storage solutions

These costs don’t show up on a settlement sheet — but they show up quickly after move-in.

9. Transactional Costs After Closing

Closing isn’t the end of transactional costs.

New homeowners often face:

Utility deposits

Trash and municipal setup fees

Minor repairs discovered after move-in

Immediate cosmetic updates

These expenses can cluster in the first 3–6 months, creating pressure if buyers haven’t left adequate cash reserves.

10. A Smarter Budgeting Framework

The goal isn’t to scare buyers — it’s to prepare them.

A more realistic ownership budget includes:

Mortgage (principal + interest)

Property taxes and insurance

Maintenance reserve

Utilities

HOA (if applicable)

A monthly buffer for irregular costs

Buyers who build this buffer upfront tend to feel far more confident — and far less stressed — after closing.

Closing Thought

The hidden costs of homeownership aren’t hidden because anyone is misleading buyers. They’re hidden because they don’t show up neatly in one place.

First-time buyers who understand these costs don’t just survive ownership — they enjoy it. They make decisions from a position of control rather than surprise, and they’re better positioned for future moves.

Owning a home is one of the most powerful financial steps you can take — as long as you budget for the whole picture, not just the mortgage.

By Eric Kelley, Philadelphia Suburbs Realtor & Attorney